2020 lookout for value added services

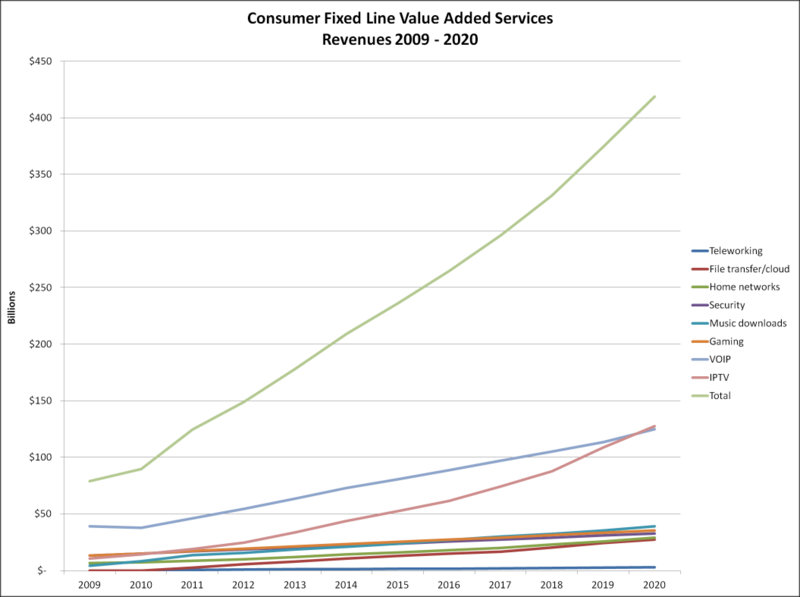

According to Oliver Johnson, CEO of Point Topic, Consumer Value Added Services (VAS) Revenues are to Triple to $420 Billion […]

According to Oliver Johnson, CEO of Point Topic, Consumer Value Added Services (VAS) Revenues are to Triple to $420 Billion […]

Companies, people, event I will be seeing (or wish I was) in London March 20-22 2012.

The main IPTV event in London was totally focussed on OTT this year.

What I am looking to get out of this year’s IP&TV World Forum

The IPTV part of triple or quad play packages has failed to be the killer-app. Might it – god-forbid- be killed off then?

Talking to French company Awox about how DLNA enables OTT to transform STB business models for operators from cash drains to cash cows