IBC 2013, impressions of a 4K OTT show

Although OTT has been an IBC topic for a few years, we actually saw a plethora of end-to-end platforms that […]

Although OTT has been an IBC topic for a few years, we actually saw a plethora of end-to-end platforms that […]

Here’s my take on what the hot topics of the IBC 2013 tradefloor – before the show:

Safe bets: 4K/UHD – HEVC – OTT (DASH Etc.) – Big Data

Outsiders: Dongles – IPTV rebirth – Targeting ads – Offloading – 4G & Fiber

In the run-up to MCW 2013, we interviewed Lonnie Schilling, newly appointed CEO of Swedish software company Birdstep Technology, that

I wrote this blog entry in planning my visit of the BBWF 2012 show floor. OTT is creating a deep

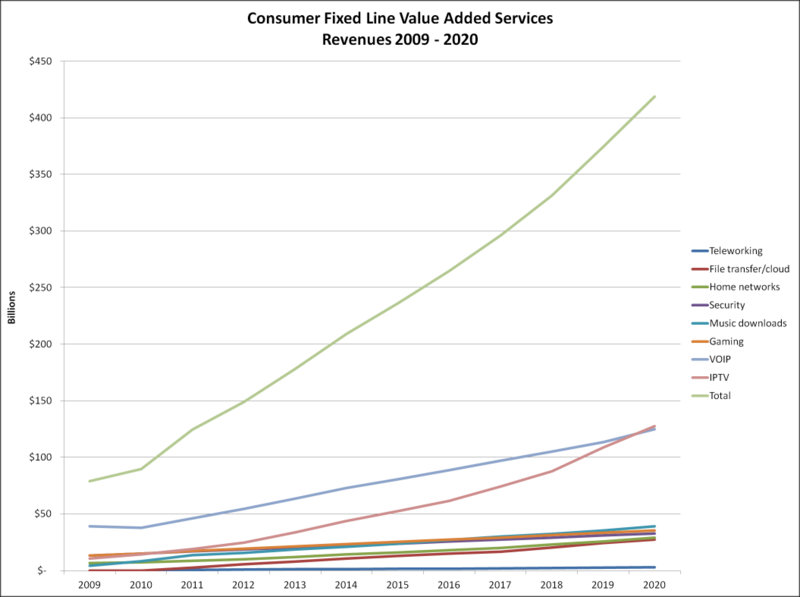

According to Oliver Johnson, CEO of Point Topic, Consumer Value Added Services (VAS) Revenues are to Triple to $420 Billion

[:en]Long version of the June 2012 Viaccess-Orca (now VO), Harmonic and Broadpeak White Paper on the technical challenges and business