Désolé, cet article est seulement disponible en Anglais Américain. Pour le confort de l’utilisateur, le contenu est affiché ci-dessous dans une autre langue. Vous pouvez cliquer le lien pour changer de langue active.

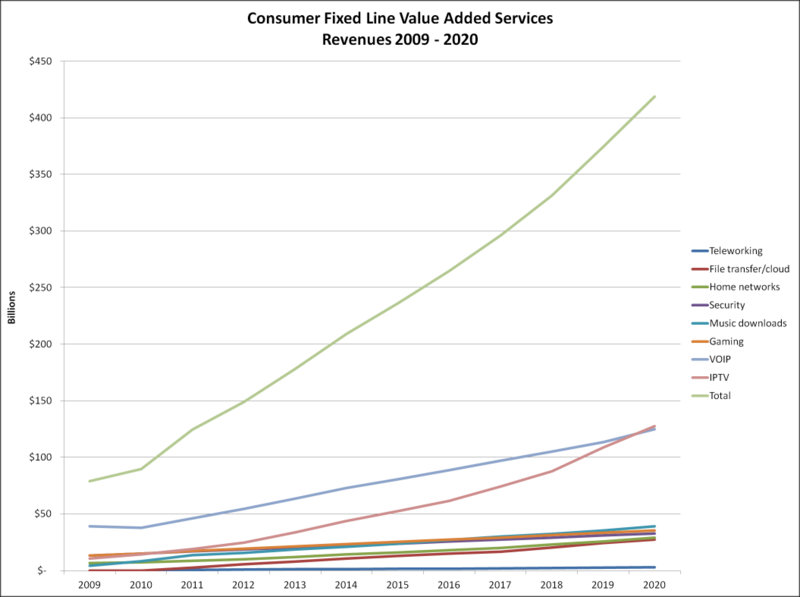

According to Oliver Johnson, CEO of Point Topic, Consumer Value Added Services (VAS) Revenues are to Triple to $420 Billion in 2020. Wow! Tripling in 10 years is a compound annual growth rate of about 14%.

Johnson used the following graphic during a presentation at CommunicAsia 2012 earlier this week:

Point Topc's take on 2020 VAS revenues

Source Point Topic (CommunicAsia 2012)

Who wouldn’t want to operate within such an industry?

That got me thinking, who indeed?

Much of what makes up these VAS aren’t yet in the scope of global juggernauts Apple & Google. On the contrary, all seem to be very Network operator centric.

So why then are my friends at major European Telcos so gloomy?

Point Topic have looked at current VAS and projected them to 2020. That’s a good approach to get an idea of market size, but doesn’t show who’ll be selling the services by 2020 i.e. in an IP lifetime.

Let’s run through Point Topic’s 8 VAS:

1. IPTV – this may still be Telco’s exclusive hunting ground but as I just wrote in a white paper, IPTV is being complemented with OTT. By 2020 there will be no distinction between IPT & OTT. If Google and Apple take too long to get their TV acts together the Netflix’ of the world will have carved out a big piece of this pie for themselves. Otherwise for Telcos to stand a chance of staying on top of this market, they’ll need the support of regulators and crazy laws like ACTA to exterminate what’s left of Net Neutrality.

2. VoIP – again what could be construed as Telco hunting ground, is already dominated globally by the likes of Skype so isn’t voice is destined to become free? I asked Point Topic to explain why they see so much VoIP revenue in 2020. Oliver told me “VoIP currently has the largest share of fixed line consumer VAS & will still grow slowly (see chart).” So what about free VoIP? “While operators are offering free VoIP, it’s often only free to other VoIP connections and sometimes only to users on the same ISP. There are still going to be plenty of calls to mobile and standard fixed phones and along with those ISPs that do charge for VoIP as part of a bundle this still adds up to a pretty good revenue stream”.

3. Gaming – Gaming is classified as just another VAS, but this industry obeys its own complex rules. Most gaming industry pundits believe that the big editors like EA or Valve will lose out to more innovative smaller outfits. Operators have been trying to capture some of the value here for over a decade. I don’t see why they should be any more successful in the future than in the past.

4. Music downloads – I’m surprised that this market is still seen as existing by Point Topic. At the last party with dancing, that I went to, people asked for a Deezer connection to play their songs, rather than hooking up their iPhone. To justify downloading, the size of files must be large relative to available bandwidth. If there are say, stereoscopic 4k videos in 2020, then maybe video downloading will still exist, but I don’t see how downloading will remain relevant for sound files in 2020. So if this revenue is generated from streaming, then network operators might just scrounge the scraps, with the lion’s share of this market remaining with service providers like iTunes or Spotify.

So I asked Point Topic why they kept this segment until 2020. Oliver answered: “streaming will become more popular, but it can still be patchy. Unless you want to use your mobile bandwidth while out of reach of free WI-FI, or eat your much larger fixed allowance then just for efficiency’s sake, users will want to download once and share that file amongst their devices. Memory/disk space if just cheaper and more reliable than having to be in the cloud the whole time. In addition we still retain the desire to 'own' something, even if it's bits on your disk drive, having something to hand is more convenient and more desirable. Just look at the Megaupload case to see what can happen to your data if you trust it to someone else.”

That’s where I beg to differ, because I think connectivity will be so much better and even more ubiquitous in 2020.

5. Security – I have no doubt that there will be a gold rush on this market. Of course anyone selling spades will make a fortune, but beyond the obvious B2B market, the jury is still out as to whether the public at large will spend significant budget on remote sensors, cameras, and the like. If the segment were to include home automation, it might stand a better chance. But it’s still a level playing field so anyone could come out on top.

6. Home networks – this is a new frontier, which I’m excited about. People are in pain and we don’t even know how to start fixing their problems. Part of the solution will include more robust and simple networking technologies, some monitoring and helpdesk services, content discovery and DLNA approaches to in-house content sharing. But if home networking can’t be made easy very soon, it may never make it as a mass market, because the Cloud is already here...

7. File transfer / cloud – I would have guessed this would be the big one in a 2020 market. Watching Dropbox make an impact in both business and consumer segments in parallel shows that there is a clear demand here. In an 8-year window I could easily imagine the descendants of Dropbox taking a slice out of whatever I’m willing to pay for access to content. Amazon seams to believe in the link between hosting services and the content therein. The experts at Point Topic have plotted a line based on today’s typical file transfer service. Again I have no issue with the method to get to a market size, but this is an area where services in 8 years will be so very different, that it probably doesn’t mean much anymore.

8. Teleworking – Teleworking was always going to be so very important so very soon. The technology has actually been available for many years. The success or otherwise of teleworking will now be driven by what is socially and / or professionally acceptable in terms of behaviour and work ethics more than by any new service or technology. So I see no reason for the tiny size or the stakeholders of the Teleworking market to change over what is - for social change - a short period of time.

Désolé, cet article est seulement disponible en Anglais Américain. Pour le confort de l’utilisateur, le contenu est affiché ci-dessous dans une autre langue. Vous pouvez cliquer le lien pour changer de langue active.

If last years theme was OTT (after a Multi-Screen show in 2010), how are we going to put 2012 into a nice neat box?

I'll gamble on the 2012 theme being something like "IPTV is dead long live OTT!"

I doubt the never-ending rumor mill on AppleTV will have an impact yet in 2012, so Apple Google & Microsoft will wait for 2013 to be main themes...

Back to the present: see you here in a few weeks to find out if I was right for 2012 at least.

2012 is set to be a very full and well attended event judging by the number of people I know that will be there. The conference tracks have become so dense that you need a day to study the program before deciding where to go. I'll just play it by ear on the day. The number of companies to see on the exhibition floor is so big anyway, that I might not be able to attend much.

IPTV has grown into a big show so there are getting to be more parties and extra add-on events.

I’ll be going to the Verimatrix "English Breakfast" on the first day which has a mini-conference on advanced video deployment (but at least I admit it it’s the English sausages that attract me).

Mariner Partner are a Canadian IPTV quality-monitoring specialist. They have a drinks party just after the first day, this year I won’t need to gate-crash as I was actually invited.

The Red Bull event later in the evening will probably be packed as usual and I’ve only got one of the tickets that are valid “until capacity is reached”, so maybe not…

On day two Irdeto is hosting a morning OTT strategy event. But I probably won’t make that one, not least because they didn’t invite me )-:

Of course day two wraps up with the glitzy prizes, this year at the London Film Museum. I went to the first 3 events as a judge, but there’s no way I will fork out £300 needed when you don’t have an invite.

I’m sure there are many more events but that’s what I’ve spotted so far.

From the list of speakers and potential prize-winners, it is clear that there will be plenty of Operators in London.

I’ll be looking to catch up with some news from Malaysia Telecom that are one of the first Huawei IPTV customers outside of China.

There’s a wrath of interesting people from Orange so I’ll be looking to get the latest form some ex-colleagues there. Also from France, I’ll try to catch up with Bouygues Telecom, which has had an amazing success story as a mobile challenger getting towards a million subs in three years. Swisscom is one of the European Telcos that is still happy with the Microsoft’s IPTV solution so I’ll tray and get some of the story there.

Paul Berriman, the veteran CTO of PCCW who launched one of the worlds first IPTV deployments in Hong Kong will be there too and it's a while since I've caught up with him.

From the trade floor my selection of vendors whose product demos I want to see include:

Whoever has cool Android boxes to show (Echostar who impressed in last year don't seem to be present).

Then Harmonic & Envivio to try and really understand how they differ.

Rovi, to actually see the demos of what I’ve been talking about for a while.

Then there is Siemens, where I want to see how their video flicking solution has fared in the market.

Zappware is a middleware alternative to NDS & Nagra. As I missed the later two at IBC I’ll try to see those demos that everyone was raving about in 2011.

Red Bee have acquired TV Genius since last year so I’ll try and find out how that’s going. There is also a new kid on the block from what I gather with Shazam moving into TV recommendation also.

I haven’t been to see Cisco in a while and they seem to have their house in order with Videoscape now so I’ll try and get an update on that too.

Ineoquest were talking a lot about ABR for OTT last year, before any of the other monitoring companies and I’d like to learn if they’ve had any success with that (as usual I, then you, will have to read between the lines because they won’t actually say directly).

I need an update on the chip maker's roadmap and ambitions in the STB space so I’ll be visiting one or more of Intel, Sigma Designs & / or STM.

I suppose you can’t blog on an event like this without talking to some of the connected TV app developers like WizzTivi.

The OTT market is already showing some results in the diaspora market so I’ll also catch up with Live Asia TV if possible.

Finally I’m due for an update on what SoftAtHome are doing.

I have some catching up, discovering to do with people that will be there without a booth. I hope to meet MediaMelon a US based CDN supplier specialized in OTT and my friends from 3 Vision, thebrainbehind, MediaTVCom, OnCubed, AppMarket.tv, etc.

Now I need to go to sleep for a couple of days, to charge up the batteries so I will actually be able to get through at least some of that ... report coming soon.

Désolé, cet article est seulement disponible en Anglais Américain. Pour le confort de l’utilisateur, le contenu est affiché ci-dessous dans une autre langue. Vous pouvez cliquer le lien pour changer de langue active.

I was expecting Over-the-top to be a prevalent theme, but not to swamp the whole conference the way it did. From the few conference talks I attended, right from the OTT Forum breakfast to Netflix’s keynote on the last day OTT was in everyone’s slides. Then on the exhibition floor there wasn’t a booth that didn’t have the precious two letters somewhere on a wall or at last in the literature.

OTT is a totally different proposition depending on which angle you take. My company is called CTO innovation Consulting, because we strive to work withall three of Content owners, Technology providers and Network Operators. So lets have a look at those three angles.

For Content owners like Hollywood studios, OTT is just another channel. In an ideal world it should represent only potential, but as Hulu pointed out at the conference, it could imply reduced margins, and if it kills off other channels it’s generally bad news. The typical knee-jerk way to fight back is to go direct to the consumer so that if there is a smaller cake to share, there are less people to share it with. Knees can jerk incredibly fast, but not much thought goes into the process.

Technology providers are eagerly rubbing their hands together in anticipation of selling new solutions. A few of the industry top guns like Apple & Google are actually changing landscape. But for the rest, be it small start-ups like the army of Connected-TV specialists, larger appliance suppliers such as encoding companies like Harmonic or Envivio, software suppliers like Adobe and even Microsoft or even OTT pure players like TVinci or Capablue it’s just one huge sales bandwagon to get on.

Now for the hardest part: Network Operators. During time of rapid broadband penetration (almost 10 years ago in developed markets, around now in emerging ones), however creative the marketers, the key selling feature has always been “as big a pipe as possible for a small a subscription as possible”. Then, as markets mature the issue becomes one of climbing up the value chain, adding value: being more than just a dumb bit pipe. OTT is a double-edged sword in this respect. It lets network operators easily access third party services and dress them up in their own colours, but it also means any other service is just a click away. This is where the Net neutrality debate comes in and it was amazingly absent from the IP&TV World forum discussions. As if the whole industry had its head in the sand. I didn’t hear a single mention of the big US operators recent decision put caps on existing data plans.

If the hype keeps up, you can expect the show to soon be rebranded OTT World forum.

I’ll be writing up my discussions on some of the booths from next week.

Désolé, cet article est seulement disponible en Anglais Américain. Pour le confort de l’utilisateur, le contenu est affiché ci-dessous dans une autre langue. Vous pouvez cliquer le lien pour changer de langue active.

Like many attendees, this year I’ll be wearing several different hats again during the show. I’ll start as a blogger and a bit of a twit (@nebul2), then put on the independent expert & analyst attire. I shall finish off the conference wearing my active IP&TV / VoD consultant’s hat.

On the exhibition floor, I’ll be milling around and peeking at everything. Last year was notable for the fancy UI demos based on Intel chipsets. This year I expect the other chipset vendors to respond. So I’m looking forward to Sigma Design’s G.hn demos and whatever is new from ST and co. I trust Pace, ADB and the other STB makers will oblige.

I’m proud to have got my 3D prediction right: last year was too early for the 3D bonanza, and it looks like this year is already late enough to avoid it again, so I don't expect to waste much more time looking at puny 3D demos.

Last year’s OTT and connected TV demos were still mostly just concepts despite several of them having already been around in 2009, but I expect to see more live services demoed this year. I’ll be especially attentive to any booths that are showing OTT services that, beyond looking desirable to the end-user, make business sense. I suppose a holy grail while going from OTT demo to OTT demo will be anything that looks like it could become a connected TV Esperanto, but that’s probably just wishful thinking; I must save some expectations for 2012’s show.

Now for the conference.

Day one: I’ll head off to the OTT breakfast hosted by an interesting ecosystem of companies, three of which I often write about. For OTT to make a difference, cooperation is central that’s why I find this initiative interesting.

Awox’s Olivier Carmona is technical marketing director of a small company with a big vision that dared to nail its colours to the DLNA mast way before it was hip.

I’m looking forward to a scheduled interview with Steve Christian of Verimatrix.

Unlike most competitors in the security business who still only really care about today’s CAS cows, Steve also gets fired up about what’s coming. He often leaves me with a “why didn’t I think of that” feeling.

Next comes Thierry Fautier who is Harmonic’s IP convergence guy. His forceful views on the way the industry is heading always take me by surprise.

Then I’m looking forward to getting the views of Minerva, Real & Heavy Reading whom I know less well but will be there too.

Thus I’ll miss the opening keynote plenary. The main conference room is usually packed with journalists so if anything interesting comes out of those presentations I’ll pick it up on twitter (@julianclover usually tweets if its really breaking news so I recommend following him as well as the #iptvwf hash tag). The only operator in the opening session is Virgin Media. IP&TV WF still has this bizarre UK focus on keynotes in spite of the fact that this is supposed to be a WORLD forum and that the UK is a long way from the centre of the IP&TV universe. As an expat Brit, I can’t help wondering if it’s an unconscious remnant of the British empire: when my Austrian grandparents got married in the 20s, they went to the centre of the world for their honeymoon, it was Nelson’s column. But that was almost a century ago.

Anyway, back to IPTV, I’ll then spend the rest of day one between the 4 conference streams and the exhibition floor.

As I’ve always been fascinated how marketing genius creates brands like Häagen-Dazs or Red Bull out of absolutely nothing, I’ll try and get to the Red Bull presentation at 3:10 in the Content stream.

Wednesday morning’s plenary seems more promising with speakers from both YouView and HbbTV, so I’ll be looking forward to some sparks flying there and a debate beyond the confines of the UK market.

If I still have fee time in the morning, I’ll be going to the Network optimisation stream, which is about adaptive rate streaming, one of my hobby horses from 2008. Huw Price-Stephens, the stream chair is probably the best chairman I’ve seen at IP&TV WF. He’s witty and provocative, so even when the speakers disappoint, he raises the standard. I’ll certainly be staying in his stream later in the afternoon, as a panellist at 15:10 on video delivery for the last mile.

I don’t know if that’s a demotion or a promotion, but for the first time, I’m not invited to the awards ceremony, which is held this year at the end of day 2. I never like Madame Tussaud’s and in any case I’ll be going to an exclusive Warner & Grey Juice screening that evening instead.

Day three will kick off for me at 8AM as I’m hosting an analyst breakfast on the commoditization of IPTV. So far we’ve had an exciting LinkedIn debate with 60 contributions so far. It came in response to a blog on the death of IPTV in France that I published on my site.

Then for much of the last day I’ll be wearing a consultant’s hat talking to clients.

I’m not too worried about missing the Google & Netflix talks during the plenary session. I’ve only ever been disappointed when listening to these big guns. Note that that may be because my expectations are set wrongly.

I’ll try and catch some of the CDN stream, which focuses on where operators are either in pain or see opportunity today as opposed to yesterday or tomorrow for the other streams.

IPTV WF have had to fight so hard to get credible speakers from the network operators (I remember being one of the first in 2004 or 2005), that now the pendulum has swung the other way: in the whole day on CDN’s almost all speakers are network operators. I’ll make a point of trying to attend the presentation from Astro, the Malaysian DTH platform at 3:30. It’s always better to start by understanding the market needs before the offers.

Then it’ll be a rush back to St Pancras station to catch a Eurostar, and hopefully write up some notes to publish here on the journey home.

Désolé, cet article est seulement disponible en Anglais Américain. Pour le confort de l’utilisateur, le contenu est affiché ci-dessous dans une autre langue. Vous pouvez cliquer le lien pour changer de langue active.

Operators seem to all copy each other in any given market; in France it is blatant.

Since Free created the 29,99€ “as much as you can eat” price-point in 2001, adding TV in 2003 content has been one of the main messages behind most ad campaigns for triple-play bundles. At least this was true until this year.

Two years ago, Bouygues Telecom came out with one of the world’s first quad play offers priced at 44,90€ per month 2 years ago, but they still only have a small TV footprint.

After a long battle, Orange, the incumbent here, gained regulatory authorization to also launch quad-play this summer.

SFR, part owned by Vodafone, is ready to launch a quad play offer, but so far has just added a VoIP to mobile option to its existing triple play and is still waiting to see how things pan out.

It has become more and more evident that Orange is moving out of content in the big exclusive way it had been pushing since 2004. In September 2010, all of Orange's 5 exclusive cinema/series channels and its Sports channel were officially put up for sale. We still don't know the outcome.

So now, as if in unison, the 3 major operators have dropped content and TV related messages from their 2010 multi-play ad campaigns.

SFR is focusing on customer service with a free Hotline. Free has also focused on a message about getting more and more service for always the same price as well as a second message about how much more (geeky) fun Free is.

Whereas Orange used to aggressively promote its own content and interactive TV features, they now only mention TV as one of many features.

IPTV is just one of many messages

The immediate conclusion to draw is that IPTV has become a commodity here. Most other mass-market commodities like water and electricity are delivered by monopolies despite the government’s best efforts to create a competitive environment. Could that mean that IPTV is one of those water-like “natural monopolies”?

But wondering about delivering say water or electricity to a household, are there any conceivable situations under which they are delivered at a loss? The answer is clearly no.

The land-grab rush for IPTV is now over and it seems we’re entering a cost control period. The official reason Orange’s new CEO Stéphane Richard gave for pulling out of exclusive living room cinema and sports, is that his company was loosing 150M€ a year on each.

What will a period of cost cutting do to IPTV? The future is all of a sudden looking a lot less clear for IPTV in France. Anyone who has actually built an IPTV business model knows that to make it float, a little creativity is required. Cost-cutters are not creative people!

It’s a moot point as to whether or not turning back is an option. Is it possible to pose the un-thinkable question for many in the industry: “could a triple-play provider, simply pull out of TV?”

One small reason for hope has a little sting in the tail.

French fibre rollout has been stopping and starting for almost five years. About a million homes are now passed. Yet only 10% of those homes are taking up a fibre service. It seems the culprit is a sluggish commercial approach from the operators. Indeed, I know there is fibre in my street in the west of Paris, but I have had no luck finding somewhere to subscribe. French operators are milking the DSL cash cow and more significantly, they haven’t yet figured how to sell fibre more expensively than DSL except to a few geeks.

The sting here is that instead of becoming the great USP to justify higher prices, the TV component for triple-play is now perceived as an expensive commodity operators have to provide, but haven’t been able to get any money from. Fibre was supposed to change all that with multiple full HD channels galore, but the wind seams to no longer be powering the sails of that dream.

We are in the age of OTT with devices available over-the-shelf that people can pick-up in the high street. France is still the most innovative IPTV market place. Despite the global 3D flop, which I saw coming before the summer (see here), the first-ever commercial 3D IPTV service was just announced in France by Dorcel for adult on demand content.

Clever operators will be those that stop trying to do it all themselves, recognize their weaknesses and concentrate on their strengths. This means building an ecosystem of suppliers where the end customer is no longer someone representing just ARPU or churn, but a stakeholder with a say in the ecosystem. It’s her living room everyone is fighting over, so give her a say. If she wants to add say an Apple-TV to her cable subscription, then make sure you help her do that. If she asks you for a hybrid box that has all the home networking features bar coffee-making, make sure you have a partner to provide one. If she only wants access to FTA channels, have a deal ready with the cheapest zapper box maker for your market.

It’s is not official yet, but my clear vision is that IPTV, as a walled garden service delivered by Telcos into the living room, is indeed dying a slow death here in France. But long live TV over IP in its many new forms. As it’s getting to be quite a jungle out there with the likes of Google entering the fray, an ISP, satellite operators or phone company close to home might be just the person needed to help cope in this brave new TV world.

[UPDATE March 11 2011] After a really interesting debate on this topic on LinkedIn, good news from the IP&TV World Forum organizers (Gavin Whitechurch). We have a slot to discuss this over breakfast in person at Olympia, Thursday 24th March 8AM. Hope you can make it.

Désolé, cet article est seulement disponible en Anglais Américain. Pour le confort de l’utilisateur, le contenu est affiché ci-dessous dans une autre langue. Vous pouvez cliquer le lien pour changer de langue active.

A connected TV powered by Awox

For the last six years, I've been going around trade shows hearing and saying that the big bad wolf in IPTV economics is the STB, which typically represents up to 70% of total capital expenditure, or CAPEX in Telco-speak.

As OTT and social media are accelerating the arrival of a new technical and business environment, my premise is that the huge threat is becoming just as big an opportunity. This year's IPTV World Forum gave me more food for thought when I spoke to Awox, which has a foot in the operator set-top box market and also a smaller one in off-the-shelf devices.

The problem

Let me go back first to the initial problem I've had to surmount several times from within operator deployments.

Typically we are talking about a total cost of ownership for a single set-top box (packaged with remote cables and CAS, delivered, installed and maintained) of, say, 150€. If we have a million subscribers the math is simple. We need a spare 10% of boxes for repairs and to ship to new subscribers so the capital required would be 165M€, all for one happy operator to pay for.

All major Telco deployments have had to cross this difficult chasm. To make things worse, IP based boxes were initially very much more expensive than satellite or cable ones. In finance terms, a way of easing the pain is to remember that contrary to head-ends, STBs are a marginal cost, which means you only pay for boxes as you deploy them to customers who hopefully are, in turn, paying for a service.

Why did all of the early operators and many coming to market today want to do something so financially bizarre as own the STB?

The first reasons were security and control.

From the outset, operators needed to obey stringent security rules set out by rights holders to be given access to their content. Before considering interactive services, an operator must at least deliver plain vanilla pay-TV. For that they must have access to the premium content that people want to watch. Therefore they must adhere to the strictest security constraints imposed by content owners. A few years ago it seemed only natural that to get into such a business, one could only play by the rules. So like cable and satellite operators, who have always owned the STB and the smartcard therein, early IPTV operators did the same and most are still doing so.

But ten years on from the launch of the first IPTV commercial trials, a consensus is appearing (there is a good Farncombe white paper on this subject here). Operators only need to own a smartcard for broadcast networks that do not have an inherent return path like satellite or digital terrestrial. For IP networks, where each STB can establish an individual link with a security server, software-based security is sufficient. A smartcard is no longer required and thus, this first reason is vanishing.

Telco’s and especially incumbents have long had a phobia about letting anything that they don’t control onto their networks. They usually have a team of security gurus who have to give a blessing before any new device can be deployed. Looking back a few decades, PTT's have always jealously guarded their PSTN networks from non-vetted devices, even plain vanilla telephones. As a teenager in the early eighties in Europe (Paris & London), I remember the thrill of plugging an illegally 'smuggled' phone from the USA. The phone was made of transparent plastic with coloured LEDs. What a thrill when at the time BT, DT or FT only supplied cream or brown handsets. In the deregulated 2010 landscape, all operators have so little control over the last mile of their networks that it seems silly to pretend that owning the STB still makes a difference, and even incumbents that own the last mile are lost when it comes to managing the home network.

Awox has experienced this gradual change first hand. They got through France Telecom’s red tape with their Internet Live-radio devices currently available to Orange subscribers in France.

Service operators have always worried about stickiness. In today's Internet world, where the competition is only a mouse-click away, it’s no surprise to Awox that many Telcos have gone for a “walled garden" approach. Indeed Awox have been through those trials and tribulations with Orange already, helping the operator offer OTT services from within their walled garden. But operators still pertain that owning the STB is part of the secret to owning the subscriber, or at least locking him or her in.

Until recently, the lack of standards has meant that operators have had to develop a new portal for most new devices. This has provided yet another argument for those proponents of a tightly controlled device policy, which again ends up meaning that operators want to own the STB.

In the early days decision-makers considered that technology was the hard nut to crack. Getting digital video through IP networks and keeping the service up and running turned out indeed to be really hard. But technological difficulties were overcome in the end and the make-or-break issue for IPTV turned out to be content and features. It's been a while since anyone has risked the tired old "content is king" slogan, but it was dominant for a long time. If that 165M€ could have been spent on content rather than STBs there might well be even more competition from IPTV operators today.

Let's leave the past there. What has changed so that 2010 might be different?

Costs can come down:

As a device vendor Awox sees itself helping move the STB away from its current CAPEX-devouring Achilles heel position, in particular through the use of standards.

Throughout the whole tech industry, standards have been the best way to lower costs. Linux Vs Windows is such an example. Awox is one of the IPTV ecosystem's DLNA champions. Olivier Carmona, the CMO, pointed out that this is particularly true for advanced home networking, for example. You can commoditize many components so that in a fully DLNA home network, for example, a low-end hard disk simply plugged into an STB becomes a ridiculously cheap NAS. Looking further down the road, Awox have contributed DTCP/IP SYNC & DTCP/IP SOURCE to the spec so that DLNA systems will be able to distribute premium content within the home. It's no longer science fiction for that same 30€ hard disk to enable PVR functionality from a DLNA enabled Pay TV service. This is yet another initiative that goes against traditional STB middleware vendors.

Other reasons:

Content owners were badly bruised from the MP3 music phenomenon - I almost wrote debacle there. However, the story is still unfolding and some musicians are living well. Musicians, like the big film studios, have now acknowledged that they must innovate. They will already agree to release content into new distribution channels and even consider entirely new business models.

Users have got used to the Internet as a source of content, even if they don't yet get premium TV from that source. They expect ready access to what is considered as free, like YouTube.

New initiatives to deliver premium content are still searching for their business models. Some, like Hulu, are bound to find some kind of stability in 2010. In the same vein, many TV stations are eager for a chance to reach out directly to the world's hundreds of millions of broadband subscribers.

In this area, the never-ending success of Apple has shown that people, beyond early adopters, will pay if the product, including digital content, is truly desirable.

Until now, TV-based widgets have been a gimmick. Indeed, if you want stock quotes in your living room you will either use your laptop, smart-phone or some tablet. But finally, demos at the 2009 IBC (more at CES, then NAB this year) are showing some really useful widgets. The secret ingredient seems to be the interactions with content itself, which NDS's Oona concept illustrates well.

Early adopters have shown that they are prepared to pay for a physical device - as long as it is desirable. Take-up of expensive devices like the Sling-box is good evidence. Some pundits predict the latest Tivo box will reinvent TV yet again in 2010.

The advent of home networks has led users to expect some control over what goes into their sitting rooms. DLNA championed by Awox will accelerate this further. Empowering users with a wider and constantly renewed choice of devices makes them happy. The marketing message is that the pain of paying is replaced by the power of choice.

Operators are scrambling to deliver sexy new 2.0 features. Big companies are rarely successful at this kind of catch-up game. I eagerly await some real figures from Verizon's much-touted Fios Twitter and Facebook implementations to see if we have reached a turning point (I heard at IPTV World Forum in March that only 10% of the user base knew about the social media features).

There are two ways of looking at the OTT box market. Some are saying that the huge variety of devices, ranging from FetchTV to Myka or Roku through Apple TV, have not yet made a huge impact. I think the glass is half full: there is such a strong a vibrant offer out there, as well as a real demand, I have no doubt that it's just a question of time - in quarters, not years - before one meets the other and we see one of the OTT services turn their huge mind-share into an equivalent market-share and then ARPU. TiVo has already shown what success can look like, albeit at a modest scale. If a box were to be operator endorsed, that could only help and the TiVo reincarnation in the UK market with Virgin backing could create a de facto standard.

Google's entry into the TV space is only a question of time. Apple, too, will eventually get it right and both giants will get a slice of the sitting room pie. Again the only sensible way forward for operators is openness, as Martin Peronnet, CEO of Monaco Telecom, pointed out during IPTV World Forum. He pointed to the way the iPhone's Appstore has diverted ARPU from operators and said, "never again".

With their internal processes, operators are never quick enough to get the time-to-market right on their own. Many big operators are publishing specifications of network API's. This is, for example, the case with the Orange Telco 2.0 initiative described by Stephan Hadinger during the last World Broadband Forum. The end game is for end users to always have the best of breed, sexiest new devices that they want enough to pay for. A lightweight certification process could guarantee that basic services all work. Any new over-the-top services would be the vendor's responsibility.

Getting rid of a huge financial burden is rewarding enough. But that 165M€ of cost discussed already could become extra revenue instead. Indeed, why would you want a better, newer device if you were not going to use it more often? Even if much of the content revenue goes to over-the-top suppliers, those extra hours will always enable some marginal revenue opportunities. Nothing stops operators jumping on to any success story as it emerges and delivering their own service, either OTT or in a walled garden. OTT services are bound to flow through different parts of the home network, where Awox' staunch DLNA support makes all the more sense.

In the model of my premise, if some technology turns out to be a dead-end, that would be the subscriber's issue. Leading-edge technology customers expect this to happen from time to time. No one sued their vendor over Betamax or HD-DVDs after all.

Sleek new devices are coming to market anyway. Operators must become better at encouraging their customers to use devices over which they still have some influence because they will not retain control for much longer.

Olivier Carmona commented that "Operators don't want the living room and it's content related revenues hijacked by an OTT supplier. Getting the sleekest, newest devices available into subscriber's sitting rooms seems a good proactive strategy". Beyond the technology, that I agree is cool, the true innovation is in the new relationship operators can have with their subscribers.

The whole industry claims the ability to link broadcast content with the interactive experience from the web. With an open standards DLNA approach, Awox believes that it is important to make only the link that best suits the user, the moment, the content and the available hardware.

Operators should consider launching new devices or peripherals to existing devices, that customers go out and buy in the stores; after all it will take them at least two years to make a decision ;o)